Third Monthly WikiLeaks Central Essay Competition | The Global Economic Crisis

THEME

The third monthly WikiLeaks Central Essay Competition 2011 solicits an answer to the question:

What are the root causes of the global economic crisis?

All sources used must be clearly identified when they occur and include the name of the source, and, when available, a hypertext link to the source content.

HOW TO ENTER

1.) If you do not already have one, register for a WLC account.

2.) Send an email to admin@wlcentral.org with the header: Competition: TITLE OF SUBMISSION by WLC ACCOUNT NAME. Insert your essay into the body of the email.

3.) See submission guidelines and rules below.

SUBMISSION GUIDELINES AND RULES

1. Eligibility/topics. The Monthly WLC Competition is open to (i) any registered member of wlcentral.org except editors and WLC essay competition judges. Regular WL Central contributors, who are not editors or judges, may enter.

a. Submissions must focus primarily on theme of the month and can be any length. Submissions must be text based (we prefer html) and emailed to admin@wlcentral.org.

b. WL Central will have the right to publish the submission without payment to the author but with attribution to the author under Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License. Please clearly indicate that your material is for publication and indicate the name you would like to appear as author. Submissions are allowed one hyperlink under the name of the author.

c. Content, previously submitted to an earlier monthly WLC essay competition, may not be again for subsequent competitions.

d. Any quotations or copyrighted material used must be properly identified. Failure to identify non-original material will result in disqualification. Each registered wlcentral.org account may enter only one entry for this month's competition. The submission must have a title.

e. Submissions can be written in any language.

2. Selection of winners. The winning essay will be selected by WL Central's editors based on (i) newsworthiness; (ii) supporting research; and (iii) organization and writing style. (iv) We will consider the essay's capacity to engender online discourse in the form of comments and retweets. The competition finalists will be published on WLC prior to the final selection. The competition winner will be notified on or about Sept 15, 2011 Sept 21, 2011, and an announcement of the winner will be sent via email to the winning entrant shortly thereafter.

3. Prize. A cash prize will be awarded for the winning essay ($US 100 US). WL Central may, in its discretion, decide to split prizes or award additional prizes.

4. Deadline for submission. All essays submitted for the competition must be received by WL Central by no later than 11:59 p.m. GMT, Sept 10, 2011.

5. In the event that none of the submissions are judged to be of suitable merit or unforeseen technical difficulties, WLC retains the right to roll the award to the next month's competition prize.

Announcing the WL Central 3rd Monthly Competition Winner | Imperium ex Nihilo

The third monthly WikiLeaks Central Competition 2011 asked writers to answer to the question: What are the root causes of the global economic crisis?

The winner is:

Authored by JP Orient

This essay was, hands down, one of the finest essays submitted to all three competitions. We encourage everyone to read it.

All the submissions were judged on (i) newsworthiness; (ii) supporting research; and (iii) organization and writing style. (iv) We also considered the submission's capacity to engender online discourse in the form of comments and retweets.

Competition Entry | Financial Collapse because of Fiat Currency, Central Banks and The Federal Reserve

What are the root causes of the global economic crisis?

by AIS

"It is well that the people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning." ― Henry Ford

Historically, many things have been used for money with the most enduring form being Gold or Silver. Paper money is largely a new idea, and the tool of scoundrels and the devious to debase the value of people's savings.

The US dollar as the World's Reserve Currency was established as such by the Bretton Woods Agreement in 1944: “The chief features of the Bretton Woods system were an obligation for each country to adopt a monetary policy that maintained the exchange rate by tying its currency to the U.S. dollar and the ability of the IMF to bridge temporary imbalances of payments”.

“On August 15, 1971, the United States unilaterally terminated convertibility of the dollar to Gold. As a result, "[t]he Bretton Woods system officially ended and the dollar became fully 'fiat currency,' backed by nothing but the promise of the federal government."

Fiat currency is simply this: The government says that something is money and must therefore be used as money. In the case of the US it is paper money and base metal coins.

The Fed essentially creates money “out of thin air”. You can find out how this is done here.

To understand the current US banking system you have to understand one completely absurd truth (at least for them), namely “debt is money”. The more debt there is, the more money a bank can “create”. The entire banking system is a complete fraud.

The central banks in other countries do primarily the same thing that the Fed does - money is created mostly by the push of a computer button and sent to banks as “loans”. There is no substance to back the money, there is no Gold backing the money - just the “full faith and credit of United States Government” which at this point looks like no faith and lousy credit.

There is no intrinsic value to any fiat currency - there is only perceived value. It is not like Gold or Silver which historically have been used for money and both are metals that people want and recognize as something which can store value. Prosperity can never come from a printing press.

An increase of the money supply by the Fed “pumping” money into the system has caused the majority of America's financial woes. For example, Greenspan pumped billions of dollars (all electronically created) into the US economy after the disaster of 9/11 which helped create a “housing bubble” of over inflated house prices that burst in late 2007 and led to the collapse of the US housing markets and was soon followed by the stock market.

David Gregory, moderator of “Meet The Press” on NBC asked Greenspan: “Are U.S. treasury bonds still safe to invest in?” Alan Greenspan, former Chairman of the Federal Reserve responded, “Very much so. This is not an issue of credit rating, the United States can pay any debt it has because we can always print money to do that. So, there is zero probability of default.”

Greenspan's comment above may sound crazy. He's right. The Fed can just keep on its rampage of inflating the money supply and pay off any debt. The problem is that when the money supply is inflated, the price of goods follows right behind it. And there comes a point in time when people demand too many dollars and thus hyper-inflation happens.

Since The Fed's inception and its control of the money supply the dollar's value has eroded by 96% of it's purchasing power from 1914. What was purchased for 4 cents in 1914 now requires $1.

As the world governments and central banks, particularly The Fed, have no substance to back the money with, that is Gold or Silver, there is no limit to how much money can be “created”. It is a vicious cycle - the more money “created out of thin air” the higher the prices of goods and the less confidence people have in the money as being a way to retain their purchasing power or savings.

The current price of Gold or Silver is a strong indication that many have no confidence in paper money and they're buying Gold and Silver it as protection against the devaluation of their wealth of fiat currency. Gold this year alone has increased in value by around 30%.

As the US had flooded the world with its debt (by borrowing money from places like China, for instance) in order to fund its wars, many countries are realizing that the US dollar is worth less and less as time goes by. They realize it would be better to not use the dollar as much, or to trade in currencies other than the US dollar.

And, it appears that the US is losing its “reserve currency” status. Several countries have directly tried to get away from the dollar and trade goods based on other currencies or commodities. Iraq, under Saddam Hussein, tried and I would suggest where that got him and Iraq. Iran is doing the same thing. They are trading their oil on the open market and receive payment in the form they want, which is not based on the value of the dollar.

The collapse is simple. The US flooded the world with its ever increasing supply of dollars which has led to a declining value of the dollar and its resulting impact upon markets. Countries want to get away from the US dollar as the reserve currency to something more stable.

The world is in a transition phase to some other standard of money. There have been talks about the use of Gold as money or the return of the US to the Gold standard but in the short term it appears highly unlikely that the “banksters” will allow anything that will interfere with their ability to create money “out of thin air”.

The control or manipulation of the money supply is too important to be left in the hands of any government or central bank. It should be left to people alone to decide what form of money they want. For example, if you want to be paid with pencils or copper pipe it's entirely your prerogative to receive such for payment.

There is no “free market” in the US. It is a completely controlled, centrally planned economy. You're not free to create a business without having to comply with countless “regulations” which are merely designed to crush creativity, prevent competition, and confiscate the wealth of those that would be so adventurous as to try and make money.

Ron Paul is the only politician in America who stands firmly against the Fed, fiat currency, and Federal spending. I believe that he has a very clear understanding of economics and why there's a business cycle of “boom and bust” and how to stop it - End the Fed, end the wars, and eliminate the US governments ability to control the money supply.

Here are what I believe are some great quotes about banking:

"I believe that banking institutions are more dangerous to our liberties than standing armies..." - Thomas Jefferson

Concerning the central bank in his time, “You are a den of vipers and thieves. I intend to rout you out, and by the grace of the Eternal God, will rout you out”. - Andrew Jackson

“I am one of those who do not believe that a national debt is a national blessing, but rather a curse to a republic; inasmuch as it is calculated to raise around the administration a moneyed aristocracy danger us to the liberties of the country”. - Andrew Jackson

"The few who understand the system, will either be so interested from its profits or so dependent on its favors, that there will be no opposition from that class." - Rothschild Brothers of London, 1863

"Give me control of a nation's money and I care not who makes it's laws" - Mayer Amschel Bauer Rothschild

"Most Americans have no real understanding of the operation of the international money lenders. The accounts of the Federal Reserve System have never been audited. It operates outside the control of Congress and manipulates the credit of the United States" - Sen. Barry Goldwater (Rep. AR)

"This [Federal Reserve Act] establishes the most gigantic trust on earth. When the President [Wilson] signs this bill, the invisible government of the monetary power will be legalized....the worst legislative crime of the ages is perpetrated by this banking and currency bill." - Charles A. Lindbergh, Sr., 1913

"From now on, depressions will be scientifically created." - Charles A. Lindbergh Sr., 1913

"The financial system has been turned over to the Federal Reserve Board. That Board as ministers the finance system by authority of a purely profiteering group. The system is private, conducted for the sole purpose of obtaining the greatest possible profits from the use of other people's money" - Charles A. Lindbergh Sr., 1923

"The Federal Reserve bank buys government bonds without one penny..." - Congressman Wright Patman, Congressional Record, Sept 30, 1941

"We have, in this country, one of the most corrupt institutions the world has ever known. I refer to the Federal Reserve Board. This evil institution has impoverished the people of the United States and has practically bankrupted our government. It has done this through the corrupt practices of the moneyed vultures who control it". - Congressman Louis T. McFadden in 1932 (Rep. PA)

"The Federal Reserve banks are one of the most corrupt institutions the world has ever seen. There is not a man within the sound of my voice who does not know that this nation is run by the International bankers - Congressman Louis T. McFadden (Rep. PA)

"Some people think the Federal Reserve Banks are the United States government's institutions. They are not government institutions. They are private credit monopolies which prey upon the people of the United States for the benefit of themselves and their foreign swindlers" - Congressional Record 12595-12603, Louis T. McFadden, Chairman of the Committee on Banking and Currency (12 years) June 10, 1932

"I have never seen more Senators express discontent with their jobs....I think the major cause is that, deep down in our hearts, we have been accomplices in doing something terrible and unforgivable to our wonderful country. Deep down in our heart, we know that we have given our children a legacy of bankruptcy. We have defrauded our country to get ourselves elected." - John Danforth (R-Mo)

"These 12 corporations together cover the whole country and monopolize and use for private gain every dollar of the public currency..." - Mr. Crozier of Cincinnati, before Senate Banking and Currency Committee – 1913

"The [Federal Reserve Act] as it stands seems to me to open the way to a vast inflation of the currency... I do not like to think that any law can be passed that will make it possible to submerge the gold standard in a flood of irredeemable paper currency." - Henry Cabot Lodge Sr., 1913

By the Federal Reserves Own Admissions:

"When you or I write a check there must be sufficient funds in out account to cover the check, but when the Federal Reserve writes a check there is no bank deposit on which that check is drawn. When the Federal Reserve writes a check, it is creating money." - Putting It Simply, Boston Federal Reserve Bank

“Neither paper currency nor deposits have value as commodities, intrinsically, a 'dollar' bill is just a piece of paper. Deposits are merely book entries." - Modern Money Mechanics Workbook, Federal Reserve Bank of Chicago, 1975

"The Federal Reserve system pays the U.S. Treasury $20.60 per thousand notes - a little over 2 cents each- without regard to the face value of the note. Federal Reserve Notes, incidentally, are the only type of currency now produced for circulation. They are printed exclusively by the Treasury's Bureau of Engraving and Printing, and the $20.60 per thousand price reflects the Bureau's full cost of production. Federal Reserve Notes are printed in 01, 02, 05, 10, 20, 50, and 100 dollar denominations only; notes of 500, 1000, 5000, and 10,000 denominations were last printed in 1945." - Donald J. Winn, Assistant to the Board of Governors of the Federal Reserve system

"We are completely dependent on the commercial banks. Someone has to borrow every dollar we have in circulation, cash or credit. If the banks create ample synthetic money we are prosperous; if not, we starve. We are absolutely without a permanent money system...It is the most important subject intelligent persons can investigate and reflect upon. It is so important that our present civilization may collapse unless it becomes widely understood and the defects remedied very soon." - Robert H. Hamphill, Atlanta Federal Reserve Bank

"By this means government may secretly and unobserved, confiscate the wealth of the people, and not one man in a million will detect the theft." - John Maynard Keynes (the father of 'Keynesian Economics' which our nation now endures) in his book The Economic Consequences of Peace (1920). [NB Keynes was a scoundrel. He means in the affirmative of what he'd like to do with those that try and save money - take it from them.

"Should government refrain from regulation (taxation), the worthlessness of the money becomes apparent and the fraud can no longer be concealed." - John Maynard Keynes, Consequences of Peace "Banks lend by creating credit. They create the means of payment out of nothing" - Ralph M. Hawtrey, Secretary of the British Treasury “A system of capitalism presumes sound money, not fiat money manipulated by a central bank. Capitalism cherishes voluntary contracts and interest rates that are determined by savings, not credit creation by a central bank." - Ron Paul “Believe me, the next step is a currency crisis because there will be a rejection of the dollar, the rejection of the dollar is a big, big event, and then your personal liberties are going to be severely threatened”. - Ron Paul “Deficits mean future tax increases, pure and simple. Deficit spending should be viewed as a tax on future generations, and politicians who create deficits should be exposed as tax hikers." - Ron Paul “I will always vote what I have promised, and always vote the Constitution, as well as I will not vote for one single penny that isn't paid for, because debt is the monster, debt is what's going to eat us up and that is why our economy is on the brink." - Ron Paul Conclusions The world's economic woes have been created and are not accidental. They are a consequence of the central banks ability to create money out of thin air. Central economic planning and controls by the governments of the world have only made things worse. There are several books and web sites which I believe will provide much more information about this entire debacle:

Competition Entry | The Institutional Power Alliance Behind the Global Economic Crisis

What are the root causes of the global economic crisis?

by chilywilly

In the past decade, the world has seen the kind of power that unaccountable institutions wield. The effects of globalization since the mid 20th century have revealed highly centralized structures of power, from financial conglomerates to pharmaceutical monopolies and oligarchic neo-corporate states.

These dominant institutions not only have extensive control over resources and capital, but make social, economic, and political decisions outside the public’s sphere of influence. Their links to one another became ubiquitously apparent during the global economic crisis of 2008, and their alliances continue to pose the greatest threat to economic stability internationally moving forward.

Extensive analyses of global institutions have been done in the past by intellectuals and by courageous journalists. Much work has been done on explaining the roles that both businesses and states have to play in what's called a market society, and their respective (and general) interests have been closely examined. The work of populous intellectuals and muckraking techniques used by whistleblowers like WikiLeaks has inspired activists in communities all around the world to socially pressure powerful institutions for various humane purposes.

But pushing society’s institutions to their limits is, by definition, not enough to significantly alter the concentrations of power inherent in the modern economy. Rather, the limits must be removed and replaced with whatever level of democracy upon which independent communities may choose. How society progresses toward that point remains in question, let alone at what rate. But understanding how far-removed and undemocratic the linkage between the corporate sectors and governments reveals an honest glimpse into the underlying causes of the economic predicament with which the world continues to struggle.

Correctly indentifying the powers inherent in the marketplace, both positive and negative, is the basis for gaining a perception of the world’s democracy deficit. The most recent major deregulation of financial markets, first suggested by former Clinton adviser Dick Morris in his arguments for ‘triangulation’ (a political strategy designed to please everyone in power, rather than just select wealthy groups), that began in 1997 is nothing more than a marginal byproduct of the rise of ‘too big to fail’ institutions.

These massive, complex institutions rose to their exceedingly obese statures in accordance with undemocratic laws dating back to the Nixon era. In the 1970s, New Deal era constraints (the Bretton Woods system) created by the US government to control capital flows were repealed, leading to the first finance-related giveaway of public-power to private financial organizations. Prior to this, massive transfers of public funds or materials (research) to private firms was done more obscurely; through tax giveaways, ‘military’ expenditures, and communities diminishing their standards by providing what businesses and the World Bank call a “better climate for investment.”

By now, private financial firms and investors had the power to regulate public finance to the extent that the free market would allow them to do so.The world would soon learn that in reality, only states could prevent the monopolization and takeover of the financial markets. Thus, one logically assumes that the state may serve as a counter-balance to the corporate systems of power. Alan Greenspan’s unremitting beliefs in the “self correcting power of free markets” combined with presidential capitulation to the corporate campaign financiers led to numerous pieces of deregulatory legislation in the late 20th century that decimated this assumption.

Reality occurred to government at the peak of 2008’s financial crisis, and the US government anxiously began pouring liquidity into the ‘private’ economy and rescuing gargantuan financial institutions from illegitimate activity. All of this was bitterly opposed by the so-called left-wing groups and right-wing tea party groups, which were unified in their public voice against the bailouts. Despite the media narrative explaining a culture of divisiveness that has just recently infiltrated America, the population was united in its opposition to an unprecedented economic role for taxpayers to play.

But the US government closely followed a record of power dynamics, the uncontroversial root of socioeconomic instability, namely that governments do not listen to their populations. This makes all the above history nothing more than a footnote, because if the public voice had been strong enough to force its position upon its rulers, there would not have been any bailout of the financial institutions. The democracy deficit, or the political distance between institutions and the people, remains the culprit for the reaction to the financial collapse.

The global economic crisis, in turn, became the end result of the public voice’s inability to scream its position loud enough to pierce the ears and hearts of those who make our decisions for us: those in power.

William Shaub (U/N: chilywilly)

Competition Entry | The Root Causes of the Global Economic Crisis

What are the root causes of the global economic crisis?

by Radioactive

These days, the most talked about news is the financial crisis that has engulfed the world economy. Everybody, the main headline of all newspapers is about falling share markets, decreasing industrial growth, high unemployment rates and the overall negative mood of the world economy (Eklavya, 2008).

The global economy crisis which is being experienced today cannot be seen as an event but rather, a process which has been building over time but has become more noticeable since September 2008 when a series of unprecedented events began to reorient the Global financial system.

These series of events has resulted in a global phenomenon called global economic/financial crisis. So what has caused this major economic upheaval in the world? What is the cause of falling share markets in the world and bankruptcy of major banks? In this essay, I intend to explain the root causes of the present day global economic crisis.

Recently, my local bank went bankrupt due to the global financial crisis. I had thought that the crisis would not reach Nigeria since we are relatively under-developed, I never knew that it was truly “global” and that even the rodents who spend some time in my room are suffering same predicament.

According to Professor Joseph Stiglitz, a Noble laureate and Professor at Columbia University, “the current financial crisis, which began in the US and then spread to Europe, has now become global” (Global Research, 2009). If you ask a thousand economists what they think is the root cause/causes of the global economic crisis, you will probably get a thousand answers! That aside, the current financial crisis is believed to have started in the United States of America where there is an imbalance in the circular flow of income.

Households and firms are the two agents in an economy. They make up the national income and national product and an economy can be in balance only if national income equals national product. However, technology improvements in two key areas, telecommunications and transportation, allowed firms in the US to outsource many design and manufacturing jobs to distant locations thus, creating an out of balance in the input and output flows.

Most of the outsourcing of labor has been to developing countries such as China and India, where labor costs are a fraction of the U.S. labor costs. As a result, China and other countries are supplying a portion of the production factors to U.S. firms that was formerly supplied by U.S. households. Money is flowing the opposite way from U.S. firms to China through the factor market.

The great imbalance arises because Chinese households are not closing the loop and buying goods and service from U.S. firms. Instead, they are hoarding most of the money, as much as 50%, and lending it to the U.S. households (Eklavya, 2008).

The U.S. households are then using the loans from Chinese savers to buy goods and services from the U.S. firms. From 2000 to 2008, U.S. households increased consumer spending, without seeing an increase in their household income. The difference has been made up with borrowed funds. In the process, the U.S. households have been building up debt which is owned to the Chinese.

This debt is in the form of credit card debt, auto loans, and the big one, home loans, which were collateralized by the U.S. housing stock. The fundamental problem is that the circular flow of income and output are out of balance. Why? Because Chinese households are selling their labor in the Factor Market, but are not buying goods in the Product Market.

For an economy to work, everyone must be both a producer and consumer. Henry Ford understood this well. His principle was that every Ford employee should afford to own a Ford automobile. If you were in Detroit during the heyday of the motor city, every car in the employee packing lot was a late mode Ford. If you go today to a Ford plant in Shanghai or Nanjing, would you see the same thing? (Eklavya, 2008).

Profligate lending, a macro-economic factor, occurred throughout all markets in the United States. The greater availability of mortgage funding predictably led to greater demand for housing, as people who couldn’t have previously qualified for credit (“sub-prime” borrowers) received loans far larger than they could have secured in the past (“prime” borrowers). When over-stretched, subprime and prime borrowers were unable to make their mortgage payments, the delinquency and foreclosure rates couldn’t be absorbed by the lenders (and those which held or bought the “toxic” paper). This undermined the mortgage market, leading to the failures of firms like Bear Stears and Lehman Brothers and the virtual failures of Fannie Mae and Freddie Mac (Wendell, 2008).

An example of how difficult the situation became in the second quarter of 2007, was when Citigroup, one the largest U.S. bank, lost U.S.$ 9,800 million committed securities because of the mortgages, whose interests were extremely.

Another possible cause of the global economic crisis lies in the compensation structure of the top executives of financial institutions. It was one based on hefty incentives and bonuses. To achieve this, they created innovative financial products that did not meet the risk-return criteria in the long run. These products were great in isolation and got great returns to the investors in the short run. However, they did not stand the test of time.

The executive’s bonuses were not based on long term returns but on short term profits. These guys made a fat pocket and there was absolutely no accountability built into the system to take care of long term failures. To further worsen issues, Auditors and Rating Agencies that supposed to monitor these companies were not ready to make public, shady dealings of these companies since these companies pay for their services (Raja world’s, 2009). You do not expect a man to bite off the fingers that feeds him.

Securitization also played a major role in spreading financial risks globally. One financial asset, such as debts, were securitized into MBSs (Mortgage Backed Securities) and CDOs (Collateralized Debt Obligations) that were sold to central banks, private banks and wealthy investment funds around the world. Virtually all major financial institutions were involved in creating and selling these products.

U.S. government sponsored enterprises, Fannie Mac and Freddie Mac, were a major source of these risky securities as they were legally required ‘to buy the “bad” subprime mortgage loans created by private lenders’. They owned or guaranteed almost half of the $12 trillion of this debt to central banks and other banks around

the world (Morrow, 2011).

Conclusively, from this essay, the basic cause of the global economic crisis is the imbalance in the U.S. circular flow of income. We can’t blame globalization but we should pondering on ways in which this imbalance can be solved. Global financial crisis could have been averted if all nations are developed. Probably what we will be hearing of will be “U.S. financial crisis” and not a global financial crisis.

This is a lesson to the governments of developing countries.

REFERENCES

- Morrow R. (2011).A critical Analysis of the U.S. Causes of the Global financial crisis of 2007-2008.

http://blog.heidi-barathieu-brun.ch/wp-archive/5239 - Eklavya (2008). Reasons for Global Recession: In plain simple English.

http://www.theindianblogger.com/problems/reasons-for-global-recession-in....

Accessed on 25 08 11 - Global Research (2009). Causes and Solutions to the Global Financial

Crisis. http://www.globalresearch.ca/index.php?context=va&aid=10792.

Accessed on 22 08 11 - Raja’s world (2009). Global Financial Crisis - Root Cause.

http://rajanvenkateswaran.blogspot.com/2009/02/global-financial-crisis-r....

Accessed on 26 08 11 - Wendell C. (2008). Root causes of the financial crisis: A primer.

http://www.newgeography.com/content/00369-root-causes-financial-crisis-a....

Accessed on 26 08 11

Competition Entry | Wie Banken Geld machen Einblicke in ein Schneeballsystem

What are the root causes of the global economic crisis?

Von Tobias Tulinus und Florian Hauschild

Im gesellschaftspolitischen Diskurs sind derzeit aus fast allen politischen Richtungen systemkritische Stimmen zu hören. "Konservative" erkennen dass "Linke" oft Recht hatten, es wird gemahnt und gewarnt, und dass der real existierende Kapitalismus nicht funktioniert, scheint mittlerweile eine Binsenweisheit geworden zu sein.

Dennoch tut die immer breitere Kritik dem derzeitigen EU-Krisenmanagement keinen Abbruch. Die europäische Elite über Merkel bis Sarkozy droht mit dem umstrittenen ESM-Vertragsentwurf das europäische Demokratie- und Transparenzdefizit nicht nur zu zementieren, sondern auch nationalstaatliche Handlungsspielräume weiter einzuschränken, so die Kritiker des so genannten Rettungsschirms.

Auch wenn generell eine koordinierte Wirtschafts- und Finanzpolitik Teil einer Währungsunion sein sollte, stellt sich doch die Frage, unter welchen Voraussetzungen und Kriterien dieser Politikwechsel nun verwirklicht werden soll.

Die öffentliche Debatte über Geld wird derweil unermüdlich geführt, doch woher Geld überhaupt kommt und wie unser Geldsystem funktioniert, wird dabei kaum erörtert. Dass der im Geldsystem verankerte Zinseszins mathematisch bedingt zu einer immer stärkeren Vermögensumverteilung führt, ist unwiderlegt. Kritiker dieser These werden zwar vereinzelt noch laut, lassen sich aber recht leicht widerlegen.

Ein weiterer bedeutender, aber viel seltener diskutierter Fehler im derzeitigen Geldsystem liegt jedoch in der gängigen Praxis der Geldschöpfung. Diese Praxis ist zutiefst ungerecht und undemokratisch. Da es ohne ein demokratisches Geldsystem auf Dauer auch keine funktionierende Demokratie geben kann, soll im Folgenden noch einmal detailliert diese Thematik vertieft werden. Aufbauend auf einem PDF der Bundesbank wird die gängige Giralgeldschöpfung umfangreich dargestellt:

Die Mindestreserve

Eine wichtige Funktion im derzeitigen Geldsystem nimmt die Festlegung einer Mindestreserve der Geschäftsbanken bei der Zentralbank ein. Diese Mindestreserve beträgt im Euroraum 2%. Die Mindestreserve muss von einer Geschäftsbank auf dem eigenen Zentralbankkonto hinterlegt werden - und zwar für das Buchgeld, das die Geschäftsbank auf den Girokonten ihrer Kunden gutgeschrieben hat.

Erzeugung von Buchgeld:

Da eine Bank also nur über 2% der von ihr gebuchten Gelder wirklich verfügen muss, ergibt sich daraus, dass die Bank Geld erzeugen oder auch "schöpfen" kann. Um einen Kredit von 10.000 Euro zu vergeben benötigt die Bank 200 Euro anderweitig nicht benötigtes Guthaben auf ihre Zentralbankkonto.

Verfügt die Bank über diese Rücklage bei der Zentralbank, kann der Kredit an den Kunden direkt vergeben werden: Dem Kunden der Bank werden also einfach 10.000 Euro auf seinem Girokonto gutgeschrieben. Geld das vorher niemand anderes besaß, es wurde durch die Kreditvergabe erst geschöpft, sprich die Information hierüber wird in die Computerdatei des Girokontos geschrieben.

Obwohl die Bank das geschöpfte Geld vor dem Kredit nicht besessen hatte, da es schlichtweg nicht existierte, ist sie nun berechtigt Zins für das neu geschöpfte und zugleich verliehene Geld zu kassieren.

Zu beachten ist auch: Analog zur Erzeugung des Buchgeldes durch Kreditvergabe wird das Buchgeld durch Kreditrückzahlung wieder vernichtet; d.h. würden (in einem theoretischen Moment) tatsächlich alle Kredite zurückgezahlt, gäbe es kein Buchgeld mehr.

Durchführung der Kreditvergabe:

Klassischerweise mussten Kreditnehmer vorweisen "kreditwürdig" zu sein. De facto wurden diese Voraussetzungen jedoch längst außer Kraft gesetzt, da Banken natürlich ein Interesse daran haben immer mehr Schuldner zu erzeugen. Privathaushalte (bspw. im Zuge der Subprime-Kreditvergabe), Unternehmen und schließlich ganze Staaten gerieten und geraten so massenhaft in die Schuldenfalle.

Aber was genau geschieht nun bei der Kreditvergabe von 10.000 Euro an einen Bankkunden? Hier gibt es verschiedene Möglichkeiten:

Fall Eins: Die Geschäftsbank verfügt auf ihrem Zentralbankkonto noch über 200 Euro, als so genannte Überschussreserve. Mit 200 Euro freiem Guthaben auf ihrem Zentralbankkonto kann die Bank wie oben beschrieben 10.000 Euro Kredit vergeben.

Fall Zwei: Die Bank nimmt einen Kredit von der Zentralbank über die 200 Euro auf und vergibt dafür einen Kredit von 10.000 Euro. Dies ist laut dem oben genannten PDF der Bundesbank der Normalfall. Für die 200 Euro zahlt die Bank den Leitzins an die Zentralbank und kassiert den weit höheren Kreditzins über 10.000 Euro vom Kunden.

Fall Drei: Ein anderer Kunde zahlt 205 Euro in bar bei der Bank ein und die Bank bucht die 205 Euro auf ihrem Zentralbankkonto ein. In diesem Fall kann die Bank dann 200 Euro Bargeld als Absicherung für den 10.000-Euro-Kredit benutzen. Die verbliebenen 5 Euro Bargeld reichen als Reserve für bis zu 250 Euro Sichteinlage des Kunden, der die 205 Euro Bargeld eingezahlt hat, welches nun zu Buchgeld auf seinem Girokonto bei der Geschäftsbank geworden ist. In diesem Fall spart die Bank die Zinsen für den 200-Euro-Kredit von der Zentralbank.

Fall Vier: Ein Kunde legt 10.000 Euro Sichteinlagen für mindestens 2 Jahre auf einem Sparbuch fest an. Dieses Geld wird dadurch zur Spareinlage und muss nicht mehr von der Mindestreserve der Bank abgedeckt werden.

Falls der Kunde das Geld allerdings bar abheben will, müsste sich die Bank 10.000 Euro Bargeld besorgen, sofern sie diese gerade nicht im Tresor hat. Das bedeutet, sie müsste im Extremfall weitere 10.000 Euro bei der Zentralbank als Kredit aufnehmen und sich in bar auszahlen lassen.

Wird nun nach der Kreditvergabe der Kredit in Höhe von 10.000 Euro als Bargeld ausgezahlt und bei einer anderen Bank wieder eingezahlt (siehe Fall Drei), könnte diese Bank dann diese Summe wieder bei der Zentralbank hinterlegen, diese 10.000 Euro, die dann wieder Buchgeld sind, mit 200 Euro Bargeld absichern, und die verbleibenden 9.800 Euro Bargeld nutzen, um 490.000 Euro Buchgeld zu schaffen.

Wie viel Geld Banken durch Kredit schöpfen können ist also auch vom Verhalten ihrer Kunden abhängig. Wenn eine Bank viele kleine Privatkunden hat, die relativ viel Bargeld abheben und wenig digitale Geschäfte tätigen wird sie relativ mehr Bargeld brauchen als eine sehr große Geschäftsbank, mit vielen Großkunden, die ihre Geschäfte meist digital abwickeln.

Verhältnis Bargeldmenge zu Buchgeldmenge:

Aus der aufgezeigten Kreditvergabepraxis ergibt sich, dass nur für einen Teil der Buchgeldmenge, Bargeld zum Auszahlen existiert. Dennoch wird von Seiten der Banken versucht, den Eindruck zu erwecken, jeder Kunde könnte jederzeit sein Geld abheben. Es liegt im Interesse der Banken Buchgeld als kongruent zu Bargeld erscheinen zu lassen. Allerdings ist nur Bargeld (also Zentralbankgeld) gesetzliches Zahlungsmittel.

Geschäftsbanken sind darauf angewiesen, dass möglichst viele Geschäfte digital getätigt werden ohne dass echtes Bargeld zum Einsatz kommt, denn eine Geschäftsbank kann nicht beliebig hohe Kredite von der Zentralbank aufnehmen. Diese müssen wiederum besichert sein. Die genauen Geschäftsgebaren zwischen Geschäftsbanken zu Zentralbanken sind jedoch sehr komplex.

Als Kunde kann man die Macht von Geschäftsbanken schmälern in dem man möglichst viel Bargeld vom eigenen Girokonto abhebt.

Tilgung des Kredits:

Da das von Beginn an tot geweihte Buchgeld durch Kreditrückzahlung wieder vernichtet wird, entsteht für die Banken ein Anreiz, die Tilgung zeitlich so weit zu verzögern wie möglich. Die von der Bank vorgeschlagene monatliche Tilgung (=Kreditrückzahlung) ist im Normalfall viel niedriger als der monatlich zu zahlende Zins. Sondertilgungen sind nicht immer möglich. Durch diese vorherige Festlegung wird es dem Kunden unmöglich gemacht, vorzeitig das Kreditverhältnis zu beenden, auch wenn er theoretisch dazu in der Lage wäre. Ziel der Banken ist es, Kunden möglichst lange in der Zinszahlungspflicht zu halten.

Das Zinssystem als weiteres ungerechtes Element des Geldsystems:

Die Erlaubnis für einen "Rohstoff" (Buchgeld), der einfach als digitale Recheneinheit geschaffen wird einen Preis (Zins) kassieren zu dürfen, ist ein Alleinstellungsmerkmal der Banken am Markt. Buchgeld zieht zudem weiteres Geld an. Wer viel hat, bekommt im bestehenden Geldsystem immer noch mehr: Geld das auf Konten oder Sparbüchern geparkt ist und verzinst wird, wird durch die Zinsen mehr und die Gesamtsumme wird dann wiederum verzinst, der so genannte Zinseszinseffekt.

Mathematisch gesehen handelt es sich hierbei um eine Exponentialfunktion: eine Kurve, die erst langsam ansteigt aber nach einigen Jahrzehnten regelrecht nach oben "explodiert". Beispiele zur Berechnung von Zins und Zinseszins gibt es hier.

Wer hingegen verschuldet ist, muss nicht nur seine Schuld abtragen, sondern auch noch die Zinsen für seinen Kredit finanzieren. Zu beachten gilt dabei auch, dass die "vollen" Konten der Einen das Rückzahlen der Schulden der Anderen erschweren bzw. unmöglich machen.

Wie oben aufgezeigt entsteht Buchgeld als Schuld. Wird Buchgeld auf einem Konto gespart und nicht mehr ausgegeben, muss die Buchgeldmenge also weiter erhöht werden, damit überhaupt an anderer Stelle die laufenden Kredite (=Schulden) bedient werden können. Dies führt zu immer neuen Schulden.

Auch die Tatsache, dass der Zins in der geschöpften Kreditbuchgeldmenge nie enthalten sein kann, führt zu immer neuen Schulden.

Der Zins muss entweder der bereits vorhandenen Geldmenge anderer Marktteilnehmer entnommen werden, oder aber wiederum durch neue Kredite finanziert werden (entweder vom Kreditnehmer selbst, oder von anderen Markteilnehmern, die ihrerseits im Wirtschaftsprozess den Beispielkreditnehmer bezahlen). Ein klassisches Schneeballsystem.

Sonderfall der Buchgeldschöpfung:

Es wird immer wieder behauptet, Banken könnten nicht einfach für sich selbst Buchgeld erschaffen. Die Bundesbank widerspricht dem eindeutig:

Zitat Bundesbank-PDF Seite 72:

"Auch kann die Geschäftsbank den Ankauf eines Vermögenswerts durch Gutschrift des Kaufbetrags auf dem Konto des Verkäufers bezahlen. Sie ist dann Eigentümerin des Vermögenswerts. Das kann beispielsweise eine Immobilie sein, die sie selbst nutzt oder die laufend Mietertrag abwirft. Bezahlt bzw. finanziert hat sie diese Immobilie mit selbst geschaffenem Giralgeld."

Fazit:

Die Buchgeldmengensteuerung über eine Mindestreserve von nur 2% (USA 10%, China 21%) bietet Banken den Ausgangspunkt zum Schaffen von neuem Geld.

Die Entstehung des Geldes als Schuld (also als laufender Kredit für den Zinsen zu entrichten sind) gepaart mit ungleicher Verteilung desselben, sorgt ebenfalls für immer neue Schulden. Hinzu kommt die Geldmenge der Zinsen, die als Preis der Buchgeldmenge nicht in ebendieser Buchgeldmenge enthalten sein kann, und somit wiederum nach Finanzierung über neue Schulden verlangt.

Mit einem solchen Blick auf die uns oft verborgenen Mechanismen im Geldsystem, lässt sich schließlich auch die Entstehung des modernen Finanzkapitalismus miterklären. Die riesigen Buchgeldmengen schreien nach Anlagemöglichkeiten. Dies ist, neben anderem, ein Grund für die Entwicklung von immer neuen Finanz"produkten".

Die Kreditvergabe durch Buchgeld dreht die entstehenden Anreize, im Vergleich zu einer Kreditvergabe aus Bargeld zwischen zwei Privatpersonen, regelrecht um: Normalerweise hätte ein Kreditgeber Interesse daran, sein Geld möglichst schnell zurück zu bekommen, weil er tatsächlich in der Zeit des laufenden Kredites darauf verzichtet, mit seinem Geld zu wirtschaften. Da Buchgeld durch Rückzahlung vernichtet wird und die Rückzahlung einfach nur das Ende des Zinsgeschäftes bedeutet, ist es im Fall der Geschäftsbanken umgekehrt.

Aus demokratietheoretischer Sicht muss das bestehende System der Buchgeldschöpfung scharf verurteilt werden, denn es handelt sich hierbei um ein oligarchisches Herrschaftsverhältnis. Als eine erste Notfallmaßnahme soll hier vorgeschlagen werden, die Lizenz zum Erschaffen von Buchgeld den Geschäftsbanken zu entziehen und in die Hände des Staates - sprich einer demokratisch organisierten Gesellschaft - zu legen.

Ebenfalls ist es möglich, parallel zum jetzigen Geldsystem, neue, basisdemokratische, kommunale, öffentliche Geldsysteme zu etablieren. Zahlreiche funktionierende Regiogelder existieren bereits. Hier ein Beispiel aus Deutschland und eines aus Brasilien.

Nach demokratietheoretischen Gesichtspunkten ergeben sich hierbei folgende Fragen:

Wieso hat der Staat Privatbanken die Lizenz zur Geldschöpfung übertragen? Die direkte Vergabe von Krediten an die öffentliche Hand durch die Zentralbank ist im Euroraum seit der zweiten Stufe der Europäischen Währungsunion von 1994 verboten, d. h. der Staat muss sich Geld bei Geschäftsbanken bzw. am Rentenmarkt leihen.

Wieso verschuldet sich der Staat - also wir alle - bei Privatbanken in Geldeinheiten, die diese schöpfen?

Wieso wird das Bereitstellen eines funktionierenden Geldsystems als größtenteils private und nicht als öffentliche Aufgabe betrachtet?

Wieso gibt es keine kommunalen, öffentlichen Banken, die ebenfalls Geld schöpfen dürften?

Die Auseinandersetzung mit diesen Fragen führen zu einer weiteren, entscheidenden Frage: Nämlich wie ohne ein demokratisches, gerechtes Geldsystem ein demokratisches politisches System und eine stabile Wirtschaftsordnung möglich sein soll. Die Frage, ob wir in einer Demokratie oder unter einer Diktatur der Finanzmärkte leben wollen, hängt zentral von der Art des Geldsystems ab, das wir nutzen.

Competition Winner | Imperium ex Nihilo

What are the root causes of the global economic crisis?

Authored by JP Orient

Abstract: This analysis argues that today's financial crisis is driven by computational heuristics, discoveries made by machines, to find logical rationales for maintaining moribund power structures. Rather than using computational heuristics to lead societies toward a world in which people desire to co-exist, the essay shows how vested interests have used machines to dictate and defend corroding centers of power. The result is an Imperium ex Nihilo, an "Empire Out of Nothing" but the assumptions of man inside the narrow focus of profit and greed.

Today's financial crisis can be analyzed through an array of lenses. In the narrowest, it is the capitulation of Keynesian economics to social conservatism emboldened by concentrated wealth. In the broadest, it represents lost trust in societies that delivered some of mankind's greatest social achievements: Enlightenment, Scientific Method, Democracy and Human Rights. Through an ecological lens we might see it as a resource-limitation shadow cast upon an ailing Earth. Militarily we may someday see the crisis as the product of imperial overreach. Commercially it could be scrutinized as a corporatist revolt, whereby organized interests overthrew the state in managing the world's tenuous plenty behind fortified castles of capital.

However history's kaleidoscope is used to see the crisis, it will be observed that the designers all used the same weapon in its proliferation: machines built to think for them.[1]

By focusing the lens on the tools of its making, today's financial crisis is seen as the betrayal of the promise that man-computer symbiosis once held. The betrayal is not wholly unexpected. Networked computing from the onset was funded and designed primarily as a tool for waging war. Its first civilian incarnation was conservative to the core. Banks used the innovation to preserve the profitability of accumulating ever more capital by reducing worker costs deployed to count wealth.

"We slaved in our underwear, in an un-air-conditioned bank vault, with an occasional six-pack of beer to make it more bearable. Every afternoon, we counted out billions of dollars of actual bond and stock certificates to be messengered to banks as collateral for overnight loans. Then, every morning, when those certificates needed for delivery to customers were returned by a group of disheveled old men who blanketed the streets of lower Manhattan carrying "bearer" bonds and stocks door-to-door, we checked them back into the firms inventory."[2]

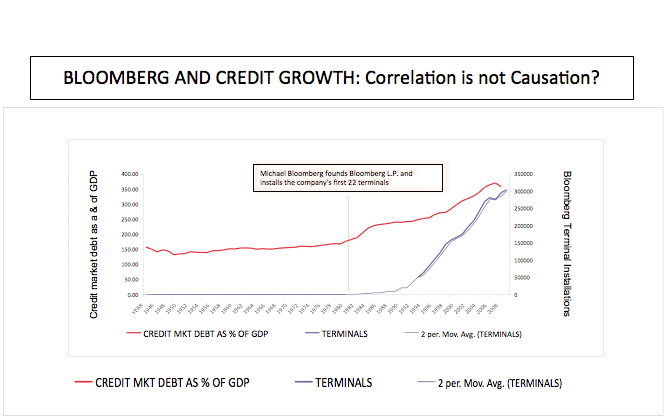

That tale of squandered youth was written by a costly 24-year-old Harvard University MBA who toiled beneath the of boilers of Solomon Brother's in 1966. His name was Michael Bloomberg. Fortunately for him, one year earlier Bank of America had hired a 42-year-old German mathematician, whose family had escaped their country's Holocaust, to alleviate the burdens of young financiers by writing a computer program to help balance the books.

"There were many very hard technical problems. It was a whale of a lot of fun attacking those hard problems, and it never occurred to me at the time that I was cooperating in a technological venture which had certain social side effects which I might come to regret. That never occurred to me. I was totally wrapped up in my identity as a professional and besides, it was just too much fun."[3]

Joseph Weizenbaum, the artificial intelligence pioneer who created, what appeared to some, a sentient machine program, ELIZA, was later recognized for his warnings that technical innovations may come at the expense of social evolution. They prop-up decaying power. Michael Bloomberg saw profit through innovation, and when released from his Solomon bond in 1981 with a $10 million check, set off to rejuvenate moribund U.S. banking with network computing.

"I would start a company that would help financial organizations ... When it came to knowing the relative value of one security versus another, most of Wall Street in 1981 had pretty much remained where it was when I began as a clerk back in the mid-1960s: a bunch of guys using No. 2 pencils, chronicling the seat-of-the-pants guesses of too many bored traders. Something that could show instantly whether government bonds were appreciating at a faster rate than corporate bonds would make smart investors out of mediocre ones, and would create an enormous competitive advantage over anyone lacking these capabilities. At a time when the U.S. budget deficit (financed by billions of dollars of new Treasury bonds and notes) was poised to explode, such a device would appeal to everyone working in finance, securities and investments..."[4]

The young investment-banking Bloomberg realized his vision and today sits atop the world's financial capital, mayor of New York and owner of the highly valuable and systemically important company bearing his name. Weizenbaum spent the last 14-years of his life in Berlin after returning disillusioned from Cambridge, MA in 1996. His ideas were documented in a film, "Plug and Pray."[5]

Source: U.S. Federal Reserve data and publicly available data on Bloomberg L.P. installations.

Bloomberg, along with other computer-aided trading and analytical networks that formed in the 1980s, benefited from more than expansionary U.S. fiscal policy. Computer processing-power costs fell, resulting in more machines inside of decision-making organizations. At the same time, computer scientists began to revolutionize software logic.

The science of heuristics -- problem-solving strategies using "rules of thumb" and intuitive guessing to detect patterns inside complex systems -- began to subsume deep modeling as a computational method to aid decision making. Whereas early network designers envisioned men using computers to deepen and refine meaning about well-understood systemic phenomena, new computational techniques ordered computers to detect patterns and meaning from seemingly incomprehensible data.[6]

Greece is ironically the etymological origin of the computational logic that financial networks tell us will be the country's ultimate demise. Heuristic is derived from the Greek word to "find" or "discover." Its root is most commonly illustrated with the story about the mathematician Archimedes who ran naked from his bathtub crying "Eureka" after solving a vexing problem. Heuristic problem-solving strategies use "fuzzy logic," "swarm intelligence" and "tabu search" algorithms. They are techniques that intuit patterns without complete information.

By the early 1980s the quintessentially human domain of seeing meaning inside the patterns of complex systems, had given way to "neural," "greedy random" and "adaptive" computer networks that identified the patterns for us. The supreme confidence in this new form of man-computer symbiosis can be glinted in the recorded tirade of Matthew Winkler, the young Wall Street Journal reporter Michael Bloomberg hired to become the public face for his financial network.

"No!" Winkler yells at a journalist who faulted a machine for an error in his reporting. "The enemy was not the computer. That's wrong. Excuse me! The enemy was not the computer. That's why we are having this meeting. I figured that a lot of you were going to think this way. It's wrong! It's not the computer, it's the human!"[7]

Caption: Mathew Winkler and Michael Bloomberg on the inside cover of "Bloomberg by Bloomberg," 1997.

Bloomberg, and similarly operated computer networks, publish the stories of machines rather than those of men. Their society has ceased to trust the discoveries, the heuristics, of man and instead turned to those calculated by machines. The result is a devastating cognitive dissonance that threatens the resiliency of societies, those patterns manifest by the fastest, deepest and most flexible processing capacity that, at times, graces the Earth: us.

Even the Defense Advance Research Project Agency, or DARPA, which funded the decades of basic research that created Internet Protocol, says that the new generation of U.S. tax-payer funded computers are a long distance from matching the human mind's raw processing power.

“We have no computers today that can begin to approach the awesome power of the human mind. A computer comparable to the human brain would need to be able to perform more than 38 thousand trillion operations per second and hold about 3,584 terabytes of memory. (IBM’s BlueGene supercomputer, one of the worlds’ most powerful, has a computational capability of 92 trillion operations per second and 8 terabytes of storage.)"[8]

It is well understood and acknowledged that languages written by man for computers necessarily contain the assumptions and biases of their authors. The "Subjective Expected Utility" model, which "defines the conditions of perfect utility-maximizing rationality in a world of certainty," has been central to economic dogma, according to a 1986 National Academy of Sciences report.[9] One of the fatal, utterly trod upon and discredited assumptions underlying virtually every financial-software heuristic is that men can be relied upon to make rational decisions.

We are reminded of the moment in "The Great Dictator" when Charlie Chaplin cries out to the soldiers "you are not machines!"[10] People experience shame. They feel guilt. They exercise compassion and love. People foment rebellion.

Our financial crisis is driven by computational heuristics, discoveries made by machines to find logical rationales for maintaining moribund power structures. Rather than using computational heuristics to lead us to a world where we want to live, societies have allowed machines to dictate and defend corroding and corrupt centers of power.

As an aside, it is noteworthy to observe how quaint the U.S. State Department cables released by Wikileaks look compared to the finance-driven headlines that define our present crisis. It is somehow touching the way U.S. public servants exercise humor, wit and drama to convey the humanity of actors balancing the scales of international order. Meta-word searches of the cables nevertheless do provide some insight into the direction our world is spinning:

- The preparation for and prevention of "war" is mentioned three times for every two that the maintenance of international "peace" is discussed.[11]

- While "Chinese" slightly overcomes "English," the focus on "Europe" surpasses "Asia" by about two-fifths.[12]

- "Democracy" is being trounced by the "bank" while "human rights" outweigh "gold" by a wide margin.[13]

- "Baseball," "Basketball," "Cricket" and "Rugby" cannot team up to match "Soccer" as a source of lively conversation around the world.[14]

The cables released by Wikileaks will keep the heuristic machines humming for a long time while they grind and churn new strategies to increase yield, extract rent, maximize profit and maintain power.

But what about the rest of us? Who among our elected leaders will speak clearly the human vision and show their guts, to man and woman alike, by exercising compassion? Who will program our machines to search for the elusive path leading to the place where peace and security overcome violence and mistrust?

Ours is an Imperium ex Nihilo, an "Empire Out of Nothing" but the assumptions of man inside the narrow focus of profit and greed. There are technical remedies that may temporarily ease the suffering that is a byproduct of machine-driven economic discoveries.[15] However in the end, we must start the long and arduous task of re-programming them to work for us, to help us see the patterns in the societies that we desire.

Our machine-made heuristics have been misappropriated. Rather than being used to minimize the risks men face in their time on Earth, they have been taken by a narrow band of craven elites who reap greater profit from the instability their discoveries sow. It is time for a clear voice human voice to say enough and bring us back into balanced alignment with our creations.

Let machine-made heuristics discover better ways to direct city traffic, guide craft in flight, and safeguard man's most deadly creation, nuclear weapons.[16]Grant them allowance to find efficiencies, safety and security. Computational heuristics can be powerful in the hands of men who know where they want to go. They are deadly inside the feckless culture of bullying that characterizes our financial institutions.

Wresting these most powerful tools of reasoning away from society's vested elites will not be easy but it is within reach. They will try to spin the counterforce of human progress against those who try. Fear. Hate. Intolerance. Nationalism. The vested elites who deploy computational heuristics, the discoveries of machines, to amass wealth have shown they are willing to support war, to turn their eyes to torture and bury habeas corpus when it is necessary to protected themselves. It will not be easy and it will not happen until humanity is exercised.

For inspiration and in parting, we might look no further than to the roots of networked computing, to the visionary JCR Licklider, who conceived of the Internet as we know it and dreamed of a day when:

"Unemployment would disappear from the face of the earth forever, for consider the magnitude of the task of adapting the network's software to all the new generations of computer, coming closer and closer upon the heels of their predecessors until the entire population of the world is caught up in an infinite crescendo of on-line interactive debugging."[17]

When at last our financial crisis is over and they finally come home, we should try to be kind to the underwear-clad bankers returning to toil by the boilers alongside the rest of us. May they bring beer.

------------------------------

[1] Technically, we may refer to these machines as "heuristically or meta-heuristically programmed computing networks"

[2] Bloomberg, Michael, "Bloomberg by Bloomberg," John Wiley & Sons, New York, 1997, page 23.

[3] ben-Aaron, Diana, "Weizenbaum examines computers and society," M.I.T.'s The Tech, Volume 105, Issue 16, April 9, 1985 (http://tech.mit.edu/V105/PDF/N16.pdf)

[4] Bloomberg, Michael, "Bloomberg by Bloomberg," pages 41-42.

[5] "Plug & Pray," 2010 http://www.imdb.com/title/tt1692889/

[6] For an exhaustive computational heuristics biography, Osman, Ibrahim H. & Laporte, Gilbert, " Metaheuristics: A bibliography" Institute of Mathematics and Statistics, University of Kent (http://sb.aub.edu.lb/PersonalSites/DrOsman/docs/Articles%20-%20pdf/BIBmh...)

For an example of applied computational heuristics, see: *Draft of *L. Ingber, M.F. Wehner, G.M. Jabbour, and T.M. Barnhill, “Application of statistical mechanics methodology to term-structure bond-pricing models,” *Mathl. Comput. Modeling *15 (11), 1991, pp. 77-98. (http://www.ingber.com/markets91_interest.pdf)

For a discussion of neural network application in finance, see: Wallace, Martin P., NEURAL NETWORKS AND THEIR APPLICATION TO FINANCE, Applied Technologies Centre, London, U.K. 2008 (http://www.saycocorporativo.com/saycoUK/BIJ/journal/Vol1No1/article_3.pdf)

For the definition of heuristics as a scientific discipline, see; Lenat, Douglas B., "The Nature of Heuristics," Xerox, Palo Alto Research Center, 1981 (http://www.bitsavers.org/pdf/xerox/parc/techReports/SSL-81-1_The_Nature_...)

[7] http://gawker.com/5002235/the-enemy-is-the-human

[8] Greenmeier, Larry, "Computers have a Lot to Learn from the Human Brain," Scientific American, March 10, 2009, http://www.scientificamerican.com/blog/post.cfm?id=computers-have-a-lot-...

[9] Simon, Herbert A.,"Decision Making and Problem Solving,"National Academy of Sciences, National Academy of Engineering, Institute of Medicine, 1986, http://www.nap.edu/openbook.php?record_id=911&page=19

[10] http://www.youtube.com/watch?v=QcvjoWOwnn4

[11] Http://www.cablegatesearch.net search for "war" on August 28, 2011 yielded 38,882 returns. The search for "peace" yielded 26,379 hits.

[12] Http://www.cablegatesearch.net search for "Chinese" on August 28, 2011 yielded 9,865; English yielded 9,417; Europe yielded 31,767; Asia yielded

18,957.

[13] Http://www.cablegatesearch.net search for "Democracy" on August 28, 2011 yielded 12,304; "Bank" yielded 26,877; "Human Rights" yielded 38,452;

"Gold" yielded 6,024.

[14] Http://www.cablegatesearch.net search for "Baseball" on August 28, 2011 yielded 247; "basketball" yielded 203; "rugby" yielded 34; "Soccer" yielded 918.

[15] This analysis does not endeavor to explore the remedies for fixing our financial crisis. For further study, UNCTAD has consistently recommended currency controls as a counter-weight to financial innovation (http://www.unctad.org/en/docs/tdr2010_en.pdf). The May 2010 "flash crash," resulting in the DJIA's biggest intraday drop, was triggered by automated, high-frequency trading programs which warrant regulatory scrutiny and oversight. At the very least, and in keeping with the spirit of the cooperative, deep-modeling that computers enable, the commands and assumptions embedded in heuristic trading algorithms should be made public through SEC or other filings. Finally, for a more traditional approach, increasing the marginal tax rate on the most highly-paid workers may encourage the physicists and computer scientists creating bank models to seek more worthwhile employment.

[16] Clarke, L.B. 1993. The Disqualification Heuristic: When do Organizations Misperceive Risk? Research in Social Problems and Public Policy 5:289-312.

[17] Licklider, JCR, "The Computer as a Communications Device," Science and Technology, 1968 (http://sloan.stanford.edu/mousesite/Secondary/Licklider.pdf)